Oil and gas industry activity in the southwestern United States continued to pick up during the fourth quarter, according to the latest Federal Reserve Bank of Dallas Survey of industry executives. Released as a report on 28 December 2017, the survey results cover the activity of companies in the US Federal Reserve System’s 11th District, which includes Texas, northern Louisiana, and southern New Mexico.

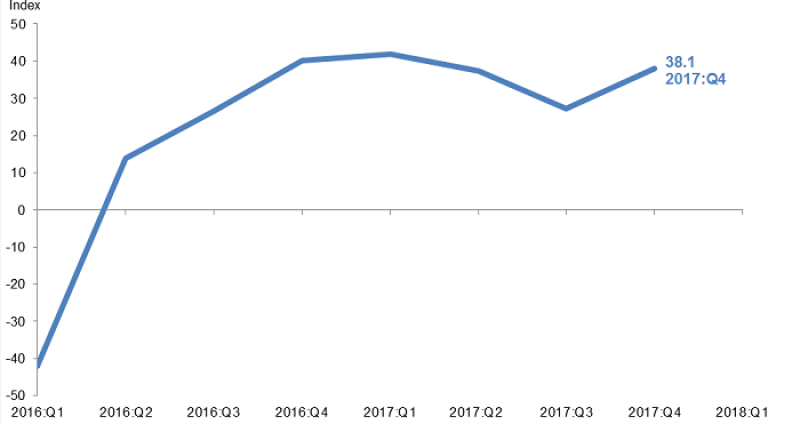

Industry operations gained momentum, with the business activity index—the survey’s broadest measure of conditions facing district energy firms—climbing from 27.3 in the third quarter to 38.1 in the most recent period (Fig. 1). Driving the increase was activity in the exploration and production (E&P) sector, the report said.

In general, positive survey readings indicate an expanding business environment, while readings below zero indicate contraction. All survey indexes reflected expansion in the last quarter.

Production Grows for Fifth Quarter

Oil and gas production increased for the fifth straight quarter, according to the survey respondents. The oil production index leaped from 19.3 in the third quarter to 33.7 in the fourth quarter. The natural gas production index rose from 17.3 to 26.6 over the same span. The increases suggest that production rose at an accelerated rate.

However, the utilization of oilfield service companies’ equipment increased at a slightly slower rate than in the previous quarter, with the corresponding index down five points at 29.6. Measures of selling prices and input costs continued to suggest some pressure on margins for oilfield service companies. The index of prices received for oilfield services remained essentially unchanged at 22.6, while the index of input costs edged up to 30.9.

Labor market indexes continue to point to rising employment and employee hours, with growth in employment primarily driven by oilfield service companies. The employment index rose nine points to 33.4 for these companies while it retreated to zero for E&P companies. The employee hours indexes showed a smaller but still sizable gap: 35.8 for service companies vs. 20.8 for E&P companies. The aggregate wages and benefits index increased from 18.4 to 25.5, the highest reading since the survey began.

Outlook Index Soars

The company outlook index posted a seventh consecutive positive reading and soared more than 20 points to 52.0 in the fourth quarter. The index measuring business outlook uncertainty declined from 4.9 to -5.3, which was its first negative reading since the index was introduced in first quarter of last year. The negative reading indicates a reduced uncertainty. The reduction was particularly prominent among oilfield service companies, for whom the uncertainty index fell to -14.3.

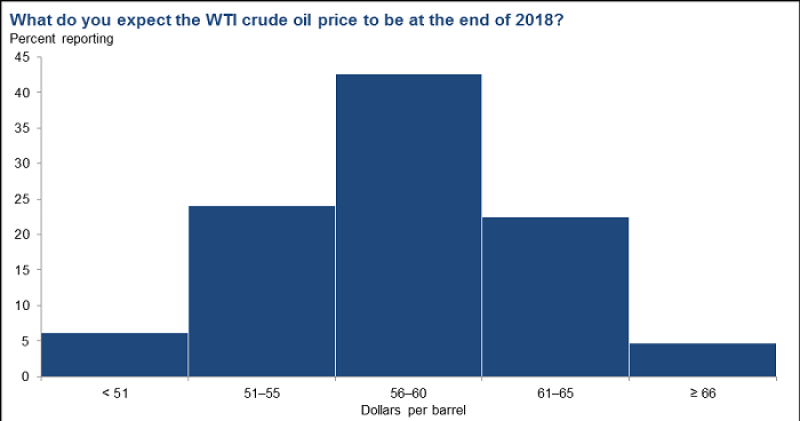

On average, respondents expect West Texas Intermediate (WTI) oil prices to be $58.98/bbl by year-end, with the estimates ranging from $45/bbl to $95/bbl (Fig. 2). Respondents expect Henry Hub natural gas prices to end 2018 at $3.05/MMBtu. For reference, WTI spot prices averaged $57.42/bbl and Henry Hub spot prices averaged $2.67/MMBtu during the survey collection period.